Home | Future Students | Financial Aid | Student Loans

Explore Student Loans at DC3

Student Loans

Student loans are serious business and should be considered carefully. The represent borrowed funds that come with a long-term financial responsibility. It’s crucial to fully understand your loan, including its actual costs like fees and interest, and the repayment timeline. Unlike grants, loans do have to be repaid. As long as you remain in school taking at least 6 credit hours you will be in an in-school deferment, and will not have to pay. Once you drop below 6 credit hours, your grace period of 6 months begins. Once your grace period ends, you will need to begin repayment of your loans.

Be a Smart Borrower!

Take time to understand the type of loan being offered to you and try to limit your borrowing to just the amounts you need to cover your expenses. You may only use the student loan money to pay for your education expenses at the school that is giving you the loan. Education expenses include school charges such as tuition, room and board, fees, and indirect expenses such as books, supplies, equipment, dependent child care expenses, transportation, and rental or purchase of a personal computer.

Know How Much You Owe!

Make sure to ALWAYS keep in contact with your loan servicer – especially if you cannot afford the payments, as there are many programs out there where they may be able to help you with payments.

If you are unsure who your lender is, sign in to www.studentaid.gov with your FSA ID (same username and password as the FAFSA) and check the loans section to find out.

Types of Federal loans – Student Loans are NOT all the same!

Direct Subsidized Loans

- Direct Subsidized Loans are awarded to students who demonstrate financial need based on the results of the Free Application for Federal Student Aid (FAFSA). The Federal Government pays the interest on this loan while a student is enrolled at least half-time (six credit hours). There is no penalty for early repayment.

Direct Unsubsidized Loans

- Federal Direct Unsubsidized Loans are not based on financial need, but a student must be enrolled at least half-time and fill out the FAFSA each year. Interest begins to accrue when the loan is first disbursed. Students can pay the interest while still in school; any unpaid interest will be added to the loan principal (capitalized) at the time of repayment. Loan capitalization can substantially increase the amount you repay. You can save money by paying the interest on an Unsubsidized loan while still in school. There is no penalty for early repayment.

Direct PLUS Loans

- A parent has the option to borrow a Parent Loan for Undergraduate Student (PLUS) for their dependent student. In addition to the student completing the FAFSA, a parent must also apply for the PLUS loan online at www.studentloans.gov.

- If a parent has been denied a PLUS loan, the parent can ask that the loan be Endorsed (adding a co-signer) or can request a credit appeal decision. The parent will be required to complete loan counseling in both instances.

- If the PLUS loan is denied, the student can request additional loan funds by completing DC3’s Additional Loan Request form.

One Big Beautiful Bill Changes

In July 2025, the way student loans are administered changed with the implementation of the One Big Beautiful Bill Act. The information that impacts our student loan borrowers can be found here at our OB3-Loan Changes page.

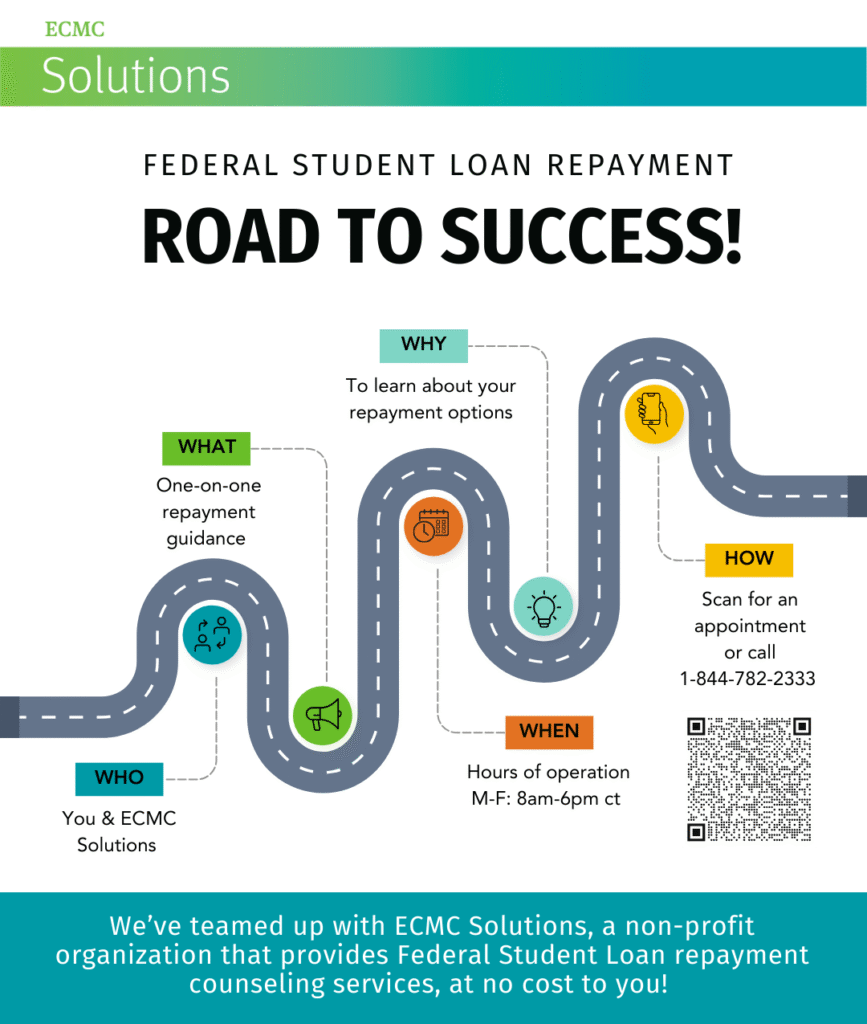

I need assistance with my student loans, repayment, loan questions, and more. Who do I talk to?

You are not alone when it comes to student loans. Dodge City Community College has partnered with Educational Credit Management Corporation (ECMC) Solutions, a nonprofit organization that provides Federal Student Loan repayment counseling services, to provide you with FREE assistance on your Federal student loan obligations to ensure successful, and comfortable, loan repayment. They assist students and families in their efforts to plan and pay for college. ECMC’s friendly customer representatives may reach out to you during your grace period to answer questions you have about your loan obligation and/or repayment options. They may also contact you if your loan(s) become delinquent. ECMC is not a collection agency. We’ve partnered with them to help you explore a wide variety of possibilities such as alternative repayment plans, deferment, consolidation, discharge, forgiveness, and forbearance options. ECMC will stay in touch with you via phone calls, letters, and/or emails to help you find answers to your questions and solutions to your issues. You are encouraged to take advantage of these free services provided by DC3!

For additional resources including information on repayment options, please visit ECMC Solutions’ Student Loan Repayment Counseling & Resources website at https://www.ecmcsolutions.org/.